The boom is over. And there are broader effects.

by Wolf Richter to Wolf Street.

Rising mortgage rates are compounding the effects of the home price explosion on mortgage payments, and it has driven layer after layer of homebuyers out of the market over the past four months. And we can see that.

Mortgage orders to buy a home have fallen further this week and are down 17% from a year ago, hitting the lowest level since May 2020, according to the Mortgage Bankers Association’s Weekly Purchase Index today. The index is down more than 30% from peak demand in late 2020 and early 2021, which was followed by a historic price hike last year.

“The drop in requisitions was evident across all loan types,” he said. MBA Report She said. “Prospective homebuyers are on the decline this spring, as they still face limited choices of homes for sale combined with rising costs from rising mortgage rates and prices. The recent drop in purchase orders is an indication of potential weakness in home sales in the coming months.”

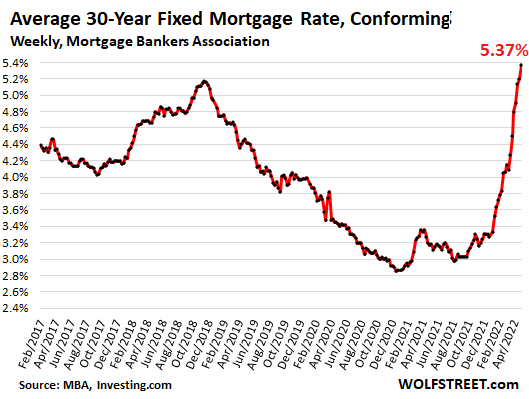

Cause of volume reduction: the toxic mixture of Housing price explosion Mortgage rates are rising. The average interest rate on 30-year fixed-rate mortgages with a 20% drop, matching the limits of Fannie Mae and Freddie Mac, jumped to 5.37%, the highest rate since August 2009, according to today’s Mortgage Bankers Association weekly gauge.

What this means for dollar homebuyers.

Mortgage on a home purchased a year ago at an average price (according to the National Association of Realtors) of $326,300, financed 20% less over 30 years, with an average price of 3.17% at the time, came with a payment of 1 320 each month.

Mortgage on a home purchased today with an average price of $375,300, minimum 20% financing, 5.37%, comes with a down payment of $990.

So today’s buyer, already suffering from rampant inflation over everything else, would have to put in an extra $670 a month — which is a 50% jump in mortgage payments — to buy same a house.

Now calculate this with homes in the more expensive areas of the country where the median price, after ridiculous hikes in the past two years, is $500,000, $1 million or more. Homebuyers face significantly higher mortgage payments in these markets.

The combination of rising home prices and rising mortgage rates has an effect on layers and classes of buyers leaving the market. And we’re starting to see that falling in mortgage applications.

The Fed caused this ridiculous housing bubble with its suppression of interest rates, including massive purchases of mortgage-backed securities and Treasuries.

The Fed is now trying to undo some of that by raising long-term interest rates. It’s the Fed’s way – too little, too late – to try to rein in the housing bubble and the risks to the financial system, which have been pushed to the limit.

What does that mean for consumer spending.

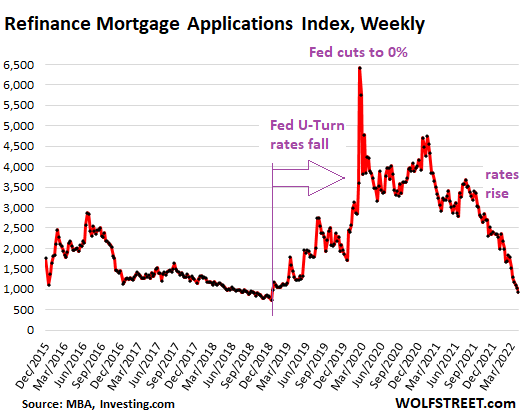

When mortgage rates drop, homeowners tend to refinance higher-rate mortgages with lower-interest mortgages, either to lower their monthly payments, withdraw cash from the home, or both.

The wave of governors that began in early 2019 as the Fed rolled out mortgage rates became infamous, and became a tsunami that began in March 2020, as mortgage rates plunged to record lows over the next few months. Homeowners lowered their monthly payments, cashing in the extra cash that the lower payments left them with. Other homeowners extracted cash by cashback and spent that money on cars and boats, and they paid their credit cards to make room for future spending, and that money was recycled in various ways and boosted the economy. Some of them are also invested in stocks and cryptocurrencies.

This effect expired months ago. So far, applications to refinance mortgages have collapsed 70% from a year ago, and by 85% as of March 2020. Refis no longer supports consumer spending, stocks, and cryptocurrencies.

What does this mean for the mortgage industry.

Mortgage bankers know that they are in a very cyclical business. In the face of rising mortgage rates, collapsing rehab demand, and declining demand for mortgage loans, the mortgage industry has begun laying off individuals.

Add Wells Fargo, one of the largest US mortgage lenders, to the growing list of mortgage lenders said to have begun layoffs late last year and so far this year, including Softbank-backed mortgage company Better.com. , but also PennyMac Financial Services, Movement Mortgage, Winnpointe Corp, and others.

Wells Fargo confirmed Last Friday’s layoffs and a statement blamed “cyclical changes in the broader mortgage lending environment,” but did not reveal the locations of the mortgage empire’s remoteness that would reduce mortgage bankers and their number.

So this boom is over. The Fed has now started raising interest rates, too little and too late, but is finally lagging forward in order to deal with this four-decade-old inflation, after 13 years of rampant money-printing – inflation of a magnitude the majority of Americans have never seen before.

Enjoy reading WOLF STREET and want to support it? Use ad blockers – I totally understand why – but would you like to support the site? You can donate. I appreciate it very much. Click on a mug of beer and iced tea to learn how to do it:

Would you like to be notified by email when WOLF STREET publishes a new article? Register here.

![]()

“Infuriatingly humble alcohol fanatic. Unapologetic beer practitioner. Analyst.”